POL: One Token for All Polygon Chains

Abstract

Abstract

This paper proposes POL, the native token of the revised Polygon protocol architecture, commonly referred to as Polygon 2.0. As the successor of MATIC, POL is envisioned to become an instrumental tool for coordination and growth of the Polygon ecosystem and the main driver of the vision of Polygon as the Value Layer for the Internet. We start by analyzing relevant work, identifying opportunities and threats and, based on that, we establish POL design goals. We propose design, utility and tokenomics of POL that achieve all the design goals. We describe the concept of the Staking Layer, a one-of-a-kind, POL-powered chain coordinator, capable of supporting a practically unlimited number of Polygon chains with arbitrary features and configurations. We believe the introduction of the Staking Layer and the wider Polygon 2.0 architecture can establish Polygon as the third most important and impactful breakthrough in Web3 (the first two being Bitcoin and Ethereum), given the magnitude of innovation and adoption it can facilitate. We introduce the Community Treasury, an in-protocol, community-governed fund designed to provide ongoing economic support for further development and growth of the Polygon ecosystem. We describe the process of migration from MATIC to POL. To analyze the proposed design, we define an economic simulation model and run simulations to confirm the hypothesis of the model, derived from the aforementioned design goals. Based on everything above, we conclude that POL is a novel, next generation asset that provides a solid foundation for the ambitious vision of the Value Layer.

Vision

Vision

The vision behind Polygon as the Value Layer of the Internet is to usher a world in which value can be created and exchanged freely and globally, similarly to how we create and exchange information today. A world which enables new – fairer, more inclusive and more efficient – forms of human organizations and governance. We strongly believe that realizing this vision can significantly advance our society. In order to make this ambitious vision a reality, Polygon’s infrastructure must improve. Specifically, it must become exponentially more scalable, without sacrificing security and user experience. To address this, a reimagined protocol architecture is being introduced as part of the Polygon 2.0 effort. This radical redesign turns Polygon into a network of ZK-powered L2 chains, unified via a novel cross-chain coordination protocol. The network can support a practically unlimited number of chains, and cross-chain interactions can happen seamlessly and instantly without additional security or trust assumptions. This design fully delivers on the aforementioned requirement – exponential scalability without sacrificing security and user experience. Figure 1. Polygon protocol architecture To coordinate, secure and grow this powerful network, an advanced, well-designed protocol economy and mechanism design are necessary. This inspired the creation of POL.

Relevant work

Relevant work

In this chapter we outline relevant native token design examples, the utility they assign to the token as well as notable advantages and disadvantages. 2.1 Bitcoin (BTC) BTC is the native token of the Bitcoin protocol, and it’s the first prominent native token implementation. The utility of BTC is twofold: ● Miner rewards: The protocol emits BTC and distributes it to protocol validators, aka miners; ● Transaction fees: Users pay fees in BTC for every transaction, which prevents spam and provides additional incentives for miners. One advantage of the BTC design is a deterministic, i.e. predictable supply. Normally, tokens with deterministic supply are more attractive to holders and can capture value better than those with non-deterministic supply. We consider BTC a legacy token design and we argue its disadvantages are multifold: ● It is an unproductive asset, it does not give its holders any meaningful role in the protocol nor the incentives to performs such a role; ● It does not leverage the opportunity to require stake in the native token for protocol validators and instead requires them to stake, i.e. invest external resources (mining equipment and electricity), thus making protocol less resilient and self-sustainable; ● It gradually reduces emission for mining rewards until it reaches zero, which introduces sustainability and security concerns (it is unclear if the security can be maintained once the emission rate becomes low or reaches zero); ● It does not introduce any type of economic support to the ecosystem; ● It does not give any governance rights to holders, although it can be argued that Layer 1 protocols such as Bitcoin should not utilize tokens for governance. 2.2 Ethereum (ETH) ETH is the native token of the Ethereum protocol and ecosystem. With its innovative design, it established the next generation of native protocol tokens.

The utility of ETH is multifold: ● Validators staking: Ethereum’s PoS (Proof-of-Stake) protocol requires validators to stake ETH in order to join the validator pool; ● Validator rewards: The protocol emits ETH and distributes it to protocol validators; ● Transaction fees: Users pay fees in ETH for every transaction, which prevents spam and provides additional incentives for validators. The design of ETH has multiple advantages: ● It is a productive asset, its holders can participate in securing the network and they receive incentives for doing that; ● It disincentivizes malicious behavior of validators via in-protocol slashing, i.e. destroying tokens of malicious validators; ● It does not introduce security and sustainability concerns, given that it doesn’t have supply cap like BTC; ● It provides economic support to the ecosystem via a predetermined portion of the initial supply allocated to the stewarding foundation. One potential disadvantage of the ETH design is that it does not have fully predictable supply, given that token emission for validator rewards increases as more tokens get staked. However, this is successfully countered by the built-in mechanism that burns1 a portion of every transaction fee, thus countering the impact of token emission for validator rewards. Another disadvantage is that the aforementioned economic support can not last indefinitely; the initial token allocation to the stewarding foundation will eventually get depleted. Lastly, it does not assign any governance right to token holders, although, as mentioned above, it can be argued that Layer 1 protocols should not utilize tokens for governance. 2.3 Cosmos (ATOM) ATOM is the native token of the Cosmos Hub, the intended central blockchain of the Cosmos multi-chain ecosystem. It has multifold utility, but only within Cosmos Hub: ● Validators staking; ● Validator rewards; ● Transaction fees; 1 https://github.com/ethereum/EIPs/blob/master/EIPS/eip-1559.md

● Governance. The design of ATOM has the following advantages: ● It is a productive asset, its holders can participate in securing Cosmos Hub and receive incentives for doing that; ● It does not introduce security and sustainability concerns, given that it doesn’t have supply cap; ● It provides economic support to the ecosystem via a predetermined allocation to the stewarding foundation; ● It gives its holders governance rights via a comprehensive governance model. The disadvantages of ATOM design: ● It only has utility within Cosmos Hub; it is not used to run and secure other chains in the ecosystem, although there are initiatives to enable this; ● It facilitates a token-only governance model, which excludes other relevant stakeholders of the ecosystem (developers, prominent contributors, applications etc.) from decision making; ● Economic support it facilitates can not last indefinitely, since the token treasury will eventually get depleted. 2.4 Polkadot (DOT) DOT is the native token of the Polkadot multi-chain ecosystem. It has the same utility as ATOM, but generally across the whole Polkadot ecosystem: ● Validators staking; ● Validator rewards; ● Transaction fees; ● Governance. The design of DOT has the following advantages: ● It is a productive asset; ● It does not introduce security and sustainability concerns, given that it doesn’t have supply cap; ● It provides economic support to the ecosystem via a predetermined allocation to the stewarding foundation; ● It gives its holders governance rights via a comprehensive governance model;

● It provides security for the whole ecosystem, i.e. all participating blockchains. The disadvantages are: ● It mandates the usage of DOT as the validator staking token for all participating chains, thus reducing architectural options for developers of Polkadot chains; ● It introduces a significant level of friction for developers of Polkadot blockchains who are required to bid and lock significant amounts of DOT in order for their chains to become part of the ecosystem; ● It facilitates a token-only governance model, which excludes other relevant stakeholders of the ecosystem from decision making; ● Economic support it facilitates can not last indefinitely, since the token treasury will eventually get depleted. 2.5 Aave (Aave) AAVE is the native token of Aave, an on-chain token lending platform. Given that AAVE is not a protocol but an application token, we do not analyze its design, advantages and disadvantages. The relevance of AAVE for POL design is twofold: ● AAVE is the successor of LEND, the initial native token of Aave; the Aave community executed a successful and beneficial migration from LEND to AAVE; ● AAVE provides its holders governance rights via a comprehensive governance model.

Design goals

Design goals

Based on the analysis of relevant work, several major opportunities for POL to benefit the Polygon ecosystem were identified. These opportunities are brought forward here as POL design goals. 1. Ecosystem security. POL should help establish a highly decentralized pool of validators that can run and secure any Polygon chain. Validators should be incentivized to join and stay in the validator pool and help secure as many chains as possible, and at the same time disincentivized to do anything malicious. 2. Infinite scalability. POL should support exponential growth of the Polygon ecosystem and eventual “hyperblochainization” of the world. Primarily, it should enable the validator pool to scale to support thousands of Polygon chains.

3. Ecosystem support. Being a global network in the making, Polygon will require ongoing economic support for further development and growth. POL should help establish a self-sustaining funding mechanism for those activities. This funding “vehicle” should be governed by the Polygon community. 4. No friction. Blockchain networks often require both users and developers to hold, stake or consume their native tokens in order to use the network. This causes friction and degrades user and developer experience. POL should be designed in a way that does not introduce any such friction. 5. Community ownership. Polygon is envisioned as a decentralized network governed by its community. Assigning governance rights to POL holders can enable creation of effective governance models in which decision makers are directly incentivized to support proposals that are in the best interest of the Polygon ecosystem.

Utility

Utility

POL is the native token of Polygon, and as such represents the major tool for coordination and incentivization of the whole Polygon ecosystem. It has multi-fold utility, namely: ● Validator staking; ● Validator rewards; ● Community ownership, i.e. governance. 4.1 Validator staking Polygon validators are required to stake POL in order to join the validator pool. Validator staking increases security of the ecosystem by: ● Preventing Sybil attacks; ● Aligning validators with the success of the ecosystem; ● Enabling slashing, i.e. punishment of malicious validators. By staking POL and joining the validator pool, validators become eligible to subscribe to validate any Polygon chain. Validation and its benefits for validators are further explained in § 6.3.

4.2 Validator rewards Decentralization and size of the validator pool is critically important for security, resilience and neutrality of the whole Polygon ecosystem. To incentivize validator onboarding and retention, predefined amounts of POL should be continuously distributed to Polygon validators as protocol rewards. Protocol rewards should be distributed to validators proportionally to the amount of POL they stake. POL emission is described in § 5.2. Protocol rewards provide base incentives for validators and establish a level playing field for the whole validator pool. On top of it, validators can then secure additional incentives by validating individual Polygon chains. Additional validator incentives are described in § 6.3. 4.3 Governance To facilitate efficient, community-run governance of important aspects of the Polygon ecosystem, POL should be technically enabled to hold governance rights, i.e. be utilized in governance frameworks. Describing the Polygon governance framework is out of the scope of this paper.

Supply

Supply

Here we cover the initial supply and the emission policy of POL, and describe the rationale behind both. 5.1 Initial supply The initial supply of POL is 10 billion tokens. The entirety of the initial supply should be dedicated for migration, i.e. token swap from MATIC to POL. This migration would need to take place in order for POL to succeed MATIC as the native token of the Polygon ecosystem, and it is discussed in § 8. The initial supply of POL matches the supply of MATIC, which should make the migration quite straightforward. Once the migration is complete, the distribution of POL would essentially match the current distribution of MATIC. MATIC has already gone through an extensive process of token distribution which has resulted in more than 600,000 holder addresses2, and likely even more 2 Source: https://etherscan.io/token/0x7d1afa7b718fb893db30a3abc0cfc608aacfebb0#balances

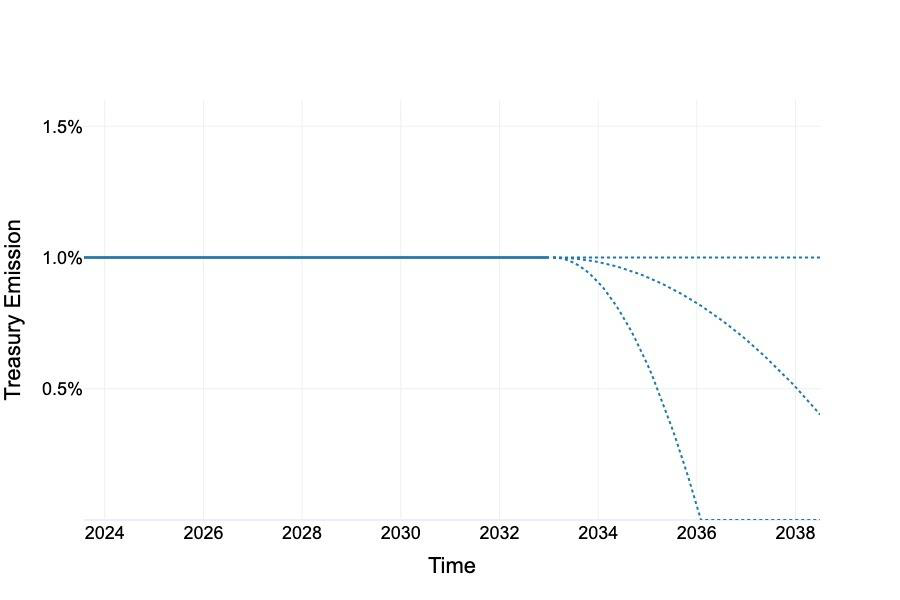

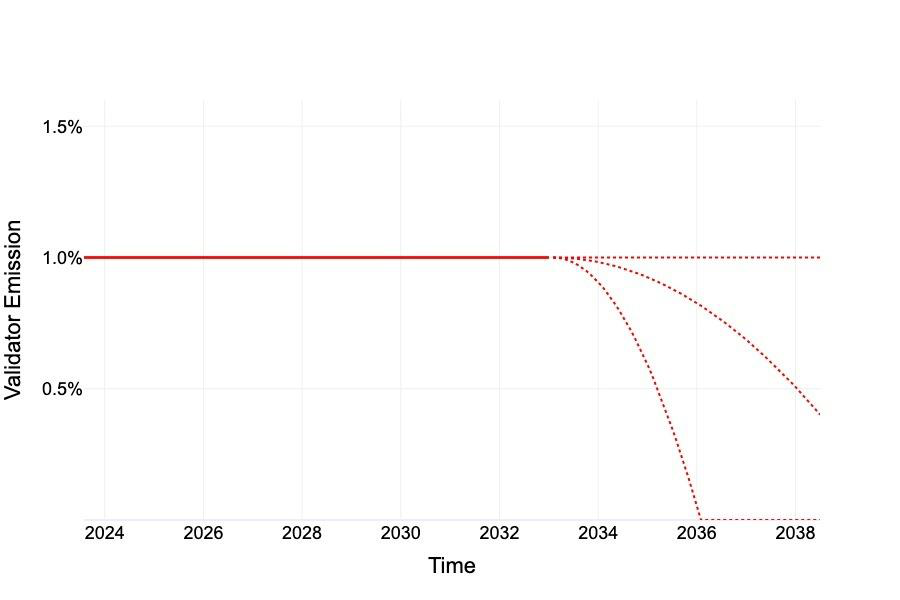

actual holders, given that centralized crypto exchanges’ and DeFi protocols’ addresses represent multiple users. This implies that POL would be widely distributed from day one, which is instrumental for overall decentralization and resilience of the ecosystem. 5.2 Emission POL is emitted at a predefined, deterministic rate for two purposes: 1. Validator rewards. To incentivize validator onboarding and retention, POL should be continuously emitted at a predetermined rate and distributed to validators as the base, protocol reward. We propose a yearly emission rate of 1% of the POL supply for this purpose. The emission rate would not be possible to change for the initial 10 years, and after that period the community can decide to decrease it in an arbitrary way via the governance framework. The emission rate can never be increased beyond 1%. 2. Ecosystem support. To provide ongoing support for further development and growth of the Polygon ecosystem, we propose to introduce the Community Treasury, a community-governed ecosystem fund, described in § 7. We propose a yearly emission rate of 1% of the POL supply for this purpose. Just like the emission for validator rewards, this emission rate can be decreased after 10 years via a governance framework, and it can never be increased beyond 1%. Figure 2. Possible POL emission rate scenarios The rationale for the proposed emission and the emission rates is that the Polygon ecosystem and Web3 in general will need time to mature and reach mainstream adoption. Based on the

historical Internet and computing platforms adoption cycles, the maturity phase could be realistically expected to happen in about 10-15 years. During that period, the ecosystem will need economic support. Once the Polygon ecosystem and Web3 reach maturity, transaction fees and other incentives secured by validating Polygon chains (described in § 6.3) should alone generate sufficient returns for Polygon validators. Once that happens, the community can decide to intervene and reduce or completely discontinue the emission for validator rewards, without impacting security and decentralization of the ecosystem. Similarly, the community can then decide to decrease or discontinue the emission for the Community Treasury as well, given that the ecosystem will not need significant economic support anymore. Obviously, the adoption cycle of Web3 might look slightly or completely different. In case it turns out that reaching mainstream adoption takes more time and the ecosystem still needs support after 10 years, the community can choose not to intervene and the emission will continue to happen for as long as required. We consider the proposed emission policy optimal, as it achieves the equilibrium between: ● Sufficient ecosystem support. Sufficient, future-proof support to the Polygon ecosystem is critically important for security and success of Polygon. To validate the hypothesis that the proposed emission rates are indeed sufficient, we developed an economic model, ran simulations and presented results in § 9. ● Security via scarcity. Scarcity of native tokens is instrumentally important for blockchain networks; high token dilution can dramatically affect security. To estimate POL scarcity, we can compare the proposed emission rate to the emission rate of BTC, which is currently at ≈1.8%3, and has been significantly higher in the past. Also, although gradually declining, BTC emission is guaranteed to happen for more than another century, whilst POL emission could potentially be reduced or discontinued even after 10 years. Given that (i) Bitcoin is considered a highly scarce asset, and (ii) total POL emission rate is comparable to (and potentially more strict than) BTC, we conclude that POL is sufficiently scarce, i.e. its emission does not introduce protocol security concerns. 3 Source: https://charts.woobull.com/bitcoin-inflation/

Lastly, it is important to note that the emission policy we propose has a high degree of predictability. The predetermined emission schedule makes POL supply predictable in the long term, even if the community decides to intervene. As explained, the community can only decrease the rates, thus effectively complementing the predetermined emission policy and potentially increasing scarcity of POL. Predictability and scarcity attract protocol and market participants and provide a sense of reliability. As the Polygon ecosystem continues to grow, this should contribute to establishing POL as an attractive and reliable digital asset, which subsequently could further ignite adoption and reliability, thus creating a virtuous circle.

Staking Layer

Staking Layer

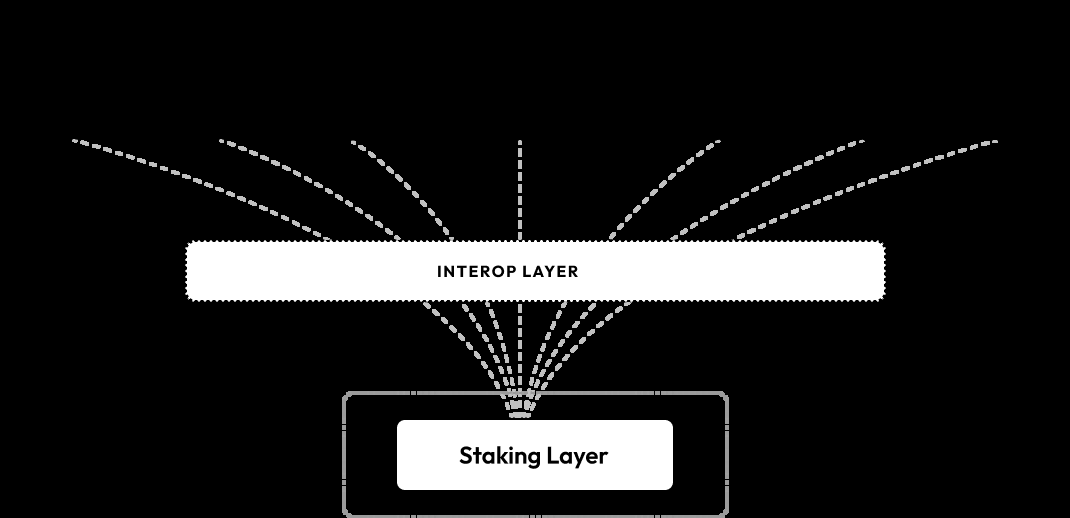

Realizing the vision of the Value Layer of the Internet will eventually require the Polygon network to host billions of users and millions of Web3 applications. To enable this vast level of activity, hundreds or thousands of Polygon chains will be running in parallel, secured by tens or hundreds of thousands of validators. In order to coordinate all Polygon chains and validators, the redesigned Polygon protocol architecture introduces the Staking Layer. The Staking Layer is a one-of-a-kind programmable multi-chain coordinator protocol. By orchestrating all Polygon validators and chains, it enables: ● Unlimited scalability of the ecosystem; ● Simple, automated access to dedicated Web3 infrastructure to any Web3 project. The Web3 industry was started by Bitcoin, the first successful blockchain with a single application – digital currency. As new applications and use cases were being proposed, they were normally launching their own blockchains, which was slow and complex. This was addressed by the second major breakthrough of Web3 – Ethereum, a programmable blockchain that can support any application or use case. Despite being a huge paradigm shift, the main limitation of Ethereum is that it is not able to scale to support mainstream adoption. To mitigate this limitation, the Ethereum community turned to Layer 2 chains – blockchain architectures that offer higher scalability without sacrificing security. With the introduction of Staking Layer, Polygon becomes capable of supporting a practically unlimited number of Layer 2 chains, each fully programmable both on the application and the configuration level. We believe this can be the third most important breakthrough since the commencement of Web3, given the magnitude of innovation and adoption it enables.

Describing and specifying the Staking Layer in detail is out of the scope of this paper. Instead, and in order to get better understanding of this POL-powered layer and its potential, we provide an overview of its following aspects: ● Design and implementation; ● Polygon chains management; ● Validator management. 6.1 Design and implementation As mentioned above, the Staking Layer is a programmable multi-chain coordinator. It manages two main logical components: 1. Validator registry: Maintains the up-to-date registry of validators, with their corresponding POL stakes and chains they are subscribed to; 2. Chain registry: Maintains the up-to-date registry of Polygon chains, with their corresponding configurations. The main feature the Staking Layer requires is full programmability; it allows it to support and coordinate: ● Arbitrary configurations of Polygon chains; ● All validator-related operations; ● Arbitrary supporting operations and applications, e.g. staking derivatives. The optimal way to achieve programmability is by utilizing EVM (Ethereum Virtual Machine), since it provides a number of benefits: ● Turing-completeness; ● Maturity of the EVM, higher level languages (e.g. Solidity) and tooling; ● Developer base etc. Practically, this means that the Staking Layer will be implemented as a set of EVM smart contracts. These smart contracts can be deployed on any EVM blockchain, likely on Ethereum or Polygon zkEVM rollup, given that both offer a high level of security. 6.2 Polygon chains management The Staking Layer can support a practically unlimited number of Polygon chains, each with arbitrary features and configuration, and provide them the required level of decentralization.

The main service that the Staking Layer provides to Polygon chains is the management of their validator requirements and validator sets established according to those requirements. Validator requirements are specified in a config smart contract that every Polygon chain deploys in order to get initiated. This smart contract can define arbitrary validator requirements, including but not limited to: ● Maximal validator number: Specifies the maximum number of validators the chain accepts in its validator set. ● Minimal validator number: The minimal number of validators required to initiate the chain. ● Slashable offenses: On-chain attributable validation offenses that cause slashing of the stake; ● Validator criteria: The only common criteria for all validators in the Staking Hub is a stake in POL. Arbitrary additional criteria can be specified, such as authorization by a third party, additional stake in other tokens (e.g. native tokens of individual Polygon chains) etc. In addition to the ability to configure validator requirements, Polygon chains can arbitrarily configure all other parameters and features of their architecture. These are not defined on the Staking Layer level, but instead in the client code of Polygon chains. Some notable parameters and features are: ● Native token: Chains can create their native tokens which can be used for various purposes, e.g. transaction fees, user incentivization etc. ● Fee management: Chains can decide how to manage transaction fees. Normally, transaction fees would be passed to validators in their entirety, but other distribution models are possible, e.g. burning a portion of fees and passing the remaining portion to validators. ● Additional rewards: All Polygon validators receive base protocol rewards (as described in § 4.2) and normally transaction fees from Polygon chains they validate. In order to attract more validators, Polygon chain can offer additional rewards on top of these. These rewards will likely often be in native tokens of those chains. ● Block time and size: It is possible to configure the frequency and size, i.e. gas limit of blocks. ● Checkpoint time: Validator sets provide fast, local finality for Polygon chains. In addition to this, all Polygon chains periodically generate and submit zero-knowledge proofs to

Ethereum, thus leveraging its high security. The frequency of these checkpoints can be configured (e.g. every 5 minutes). ● Data availability: The data availability model can also be specified. Chains can decide to leverage Ethereum (rollup model) or their own validator sets or other external data availability service (validium model). With the proposed framework, launching a new Polygon chain practically boils down to writing and deploying the aforementioned config smart contract. Once the contract gets deployed to the Staking Layer, validators can start subscribing to it. When the minimal required number of validators is reached, the chain gets launched. We believe that this simple way of configuring and launching chains can usher a new era of innovation and adoption. The game-changing design decision of Ethereum was to not try to predict what applications and use cases developers will want to build. Instead, it offered a Turing-complete programmable environment that can support any application or use case. With the Staking Layer, Polygon is taking the same approach for launching new chains – it supports practically any chain design, in a programmable manner and without scaling limitations. 6.3 Validator management The Staking Layer can support a practically unlimited number of validators. It manages validators throughout their whole lifecycle and enables them to secure different types of incentives for performing useful work. There are four possible phases, i.e. statuses, in the validator lifecycle: 1. Activation: Validators get initiated as part of the validator pool by depositing POL into the staking contract on the Staking Layer. Once initiated, validators become eligible to receive base protocol rewards (described in § 4.2). 2. Subscription: Once initiated, validators are allowed to subscribe to validate any Polygon chain. 3. Validation: If a validator meets all the criteria of the Polygon chain it subscribed to, it becomes a member of that chain’s validator set. Validators can validate multiple chains, and their POL stake is acknowledged on each of those chains. If a validator gets slashed for a predefined slashable offense on one of the chains, its POL balance gets updated and reflected on all chains it validates. The validation and subscription phases can

overlap; a single validator can be in the subscription phase on one Polygon chain and in the validation phase on another. 4. Retirement: Validators can leave the validator pool at any point. Once the retirement is initiated, a predefined waiting period commences, allowing for potential pending slashing. After the waiting period, validators are able to withdraw their POL stake from the deposit contract. In return for validating Polygon chains, validators can establish at least three incentive streams: 1. Protocol rewards: As described above, every active Polygon validator is receiving base protocol rewards. The total POL emission for validator rewards (described in § 5.2), is distributed to active validators proportionally to their POL stake. 2. Transaction fees: Validators are allowed to validate any number of Polygon chains. In return, these chains will normally award the entirety or a portion of transaction fees to validators. 3. Additional rewards: As mentioned above, some Polygon chains can choose to introduce additional rewards to attract more validators. These rewards can be in any token, including but not limited to POL, stablecoins or native tokens of those Polygon chains. As we describe validator incentives, it is worth noting that the concept of validation in Polygon is broader than the usual, narrow definition. This further improves the value proposition of the validator role – in addition to validating multiple chains, validators can also perform multiple roles on a single chain. The most common roles will likely be: ● Validation in the narrow sense: Accepting user transactions, determining their validity and generating blocks; ● Proving: Producing zero-knowledge proofs of transaction validity; ● Data availability: Providing guarantees that transaction data is published and publicly available.

Community Treasury

Community Treasury

The Polygon ecosystem and the whole Web3 industry are still in the early adoption and heavy development phase. To remain on the current growth trajectory, the Polygon ecosystem will need ongoing economic support in years to come.

To address the need for ongoing ecosystem support, we propose the Community Treasury, an in-protocol, community-governed ecosystem fund. It introduces at least three major benefits to the Polygon ecosystem: ● Ongoing, self-sustainable economic support for as long as required; ● Increased decentralization by reducing dependency on the Polygon Foundation; ● Achieving the next level of transparency and community inclusion. As described in § 5.2, the Community Treasury is funded by a predetermined emission of POL. The emission rate dedicated to this purpose is 1% per year, or ≈100 million POL in absolute terms, and can not be changed for 10 years. This guarantees strong ecosystem support during this period, critical for development, growth and positioning of Polygon. Once the Polygon ecosystem and Web3 reach maturity, the ecosystem will likely not need significant economic support anymore. At that point, the community should intervene and decrease or discontinue the emission for the Community Treasury. In an optimistic scenario, where maturity is reached before the 10-year period of guaranteed funding expires, the Community Treasury might end up having more funds than the ecosystem realistically needs. In that case, the community should decide how to utilize this excess POL. For example, a decision can be made to burn it. As mentioned, and as the name indicates, the Community Treasury should be governed by the community, via an agreed upon governance process. The governance process and the wider Polygon governance framework are being designed and established as part of the Polygon 2.0 effort, and explaining them in detail is out of the scope of this paper. Instead, we give a brief overview of its two likely concepts: 1. Polygon Funding Proposals (PFPs): Formal proposals for funding or other activities or improvements related to the Community Treasury. PFPs can be submitted by anyone, and should be publicly available and discussed. Similar concepts can be observed in other prominent governance frameworks4,5. 2. Consensus gathering: The process of making a decision on a specific PFP. The decision can be made in a direct manner, where every community member can participate, or via delegates who represent the community. As mentioned in § 4.3, POL should be technically enabled to hold governance rights, so it can potentially be utilized 5 https://docs.aave.com/governance/ 4 https://uniswap.org/governance

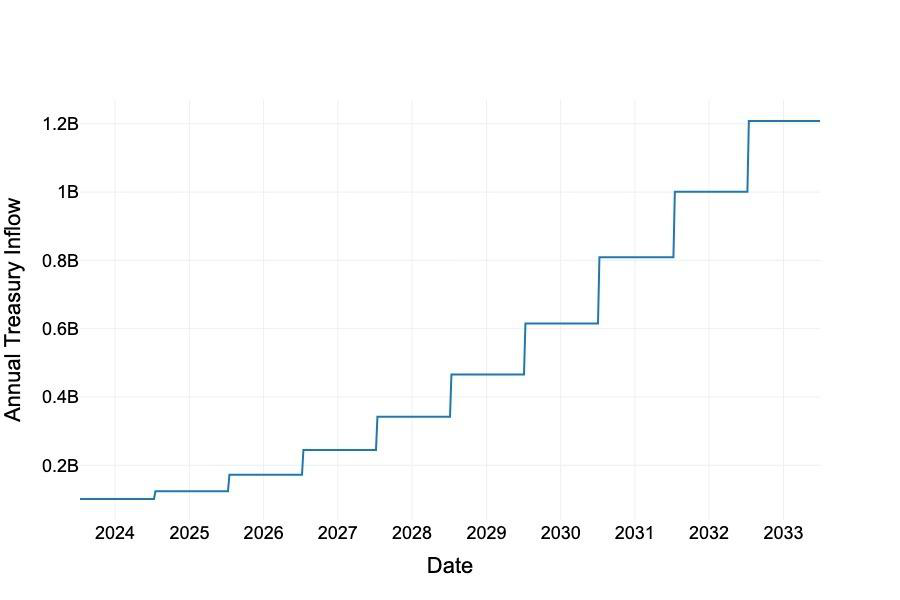

as part of the consensus gathering or the delegate election process. POL holders are directly economically incentivized to approve good proposals and reject the bad ones, which makes the decision making process more likely to benefit the ecosystem. We simulated ongoing Community Treasury inflows in § 9.

Migration

Migration

Given that POL is being proposed as the successor of MATIC, the current native token of Polygon, migration from the old to the new token would need to take place. The initial supply of POL proposed in § 5.1 matches the current supply of MATIC and was proposed to simplify the migration process as much as possible. For self-custodying MATIC holders, the migration would require a simple action – swap from MATIC to POL, using the swapping smart contract that should be created for that purpose. The swapping contract should accept MATIC from any address and return the equivalent amount of POL to the same address. For MATIC holders who keep their tokens with centralized crypto exchanges and custodians, the migration would normally be automatic, i.e. would not require any action. Every MATIC holder should be able to swap their tokens for POL, including those who have MATIC “locked” for multiple years in various DeFi or vesting contracts, or the uninformed holders who find out about POL at some point in the future. For this reason, the migration should be allowed to happen during a prolonged period of time (e.g. 4 years), if not indefinitely. The migration should be voluntary, i.e. it cannot be forced. However, if POL is accepted by the majority of the community as the new native token, there will be little to no reason to hold MATIC instead of POL. In this situation, it is reasonable to expect that the migration will practically be fully executed, i.e. the vast majority of MATIC will be migrated.

Model

Model

Based on the design of POL and the Staking Layer, we propose a model to simulate important performance indicators of the POL-powered ecosystem, provide required inputs and analyze the results of simulations.

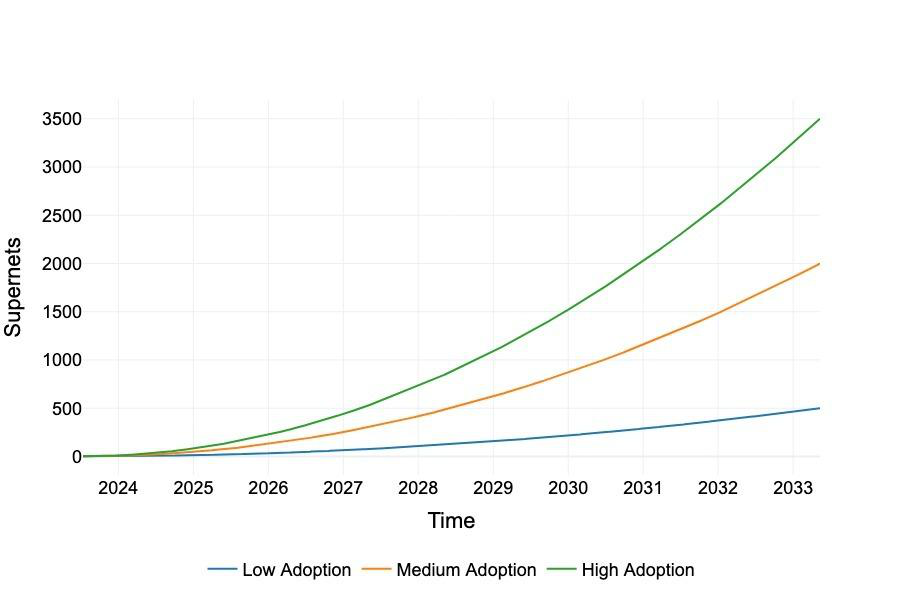

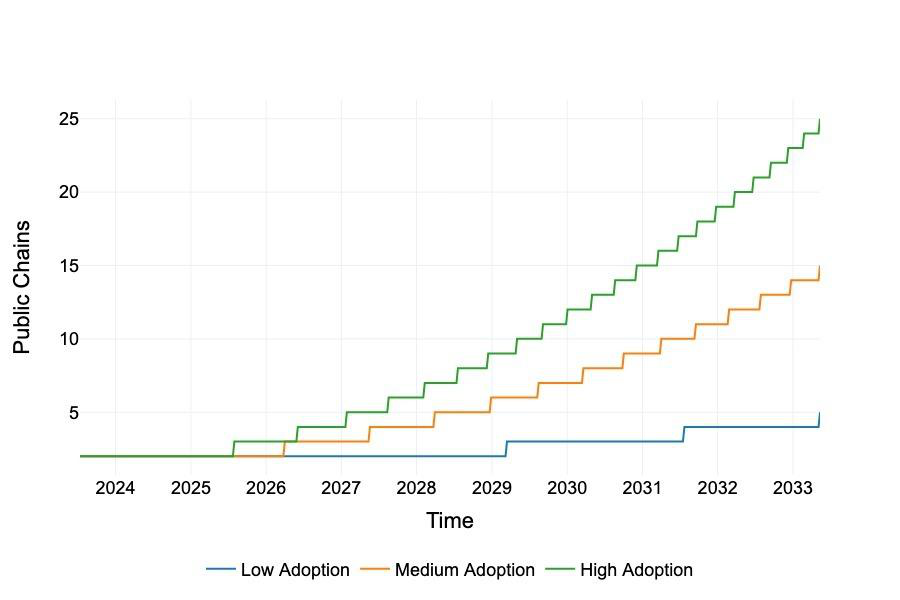

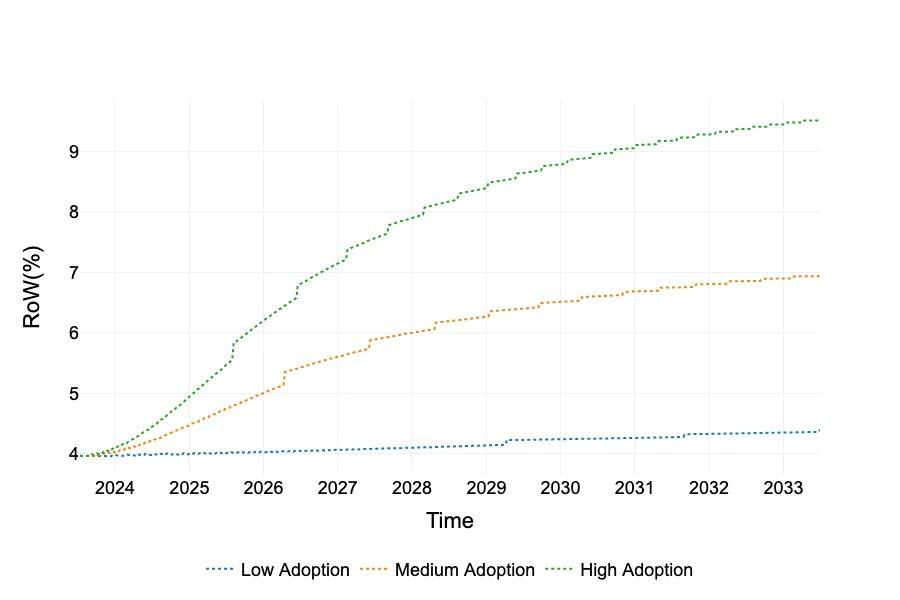

9.1 Hypothesis The purpose of the model is to validate the hypothesis that the proposed POL-powered ecosystem can simultaneously meet the following goals, derived from § 3: ● Sufficient ecosystem security: We measure security through POL staking ratio, i.e. percentage of the POL supply staked by validators. The minimal satisfactory ratio is 30-40%, roughly equivalent to the current staking ratio on the Polygon PoS chain6. ● Sufficient validator incentives: To estimate sufficiency of validator incentives, we introduce Return on Work (ROW), the measure of total validator earnings relative to the value of staked POL. The minimal satisfactory return is 4-5%; lower returns are not considered attractive enough, considering the work being performed, the risks and the opportunity costs. ● Sufficient ecosystem support: We measure ecosystem support through yearly inflow to the Community Treasury. The minimal satisfactory inflow is $50-100 million, and it is determined based on the current level of economic support the Polygon ecosystem needs. We explicitly define these indicators (staking ratio, validator returns and treasury inflow) in § 9.3. 9.2 Inputs In this chapter we outline the required model inputs and estimate their respectable values. First, we define three growth scenarios, projecting the abstract number of chains in the Polygon ecosystem during the initial 10-year period. We refer to the number of chains as abstract because it is not necessarily expressing the exact number of Polygon chains (although that might be the case), but more the cumulative level of activity, i.e. transactions in the ecosystem. 6 Source: https://staking.polygon.technology/

Figure 3. 10-year growth scenarios The rationale for the growth scenarios is based on the following data and observations: ● Current growth trajectory. Since the inception in 2020, the Polygon ecosystem has grown to thousand of applications and 3 million daily transactions7. If this trend even remotely continues, the proposed growth scenarios seem realistic. ● Web2 app marketplaces: The App Store hosts around 1.8 million applications8 and Google Play around 2.7 million9; both were introduced around 14 years ago. It could be reasonable to expect a comparable level of adoption for Web3 in a comparable timeframe. ● Supernets adoption: At the moment of writing this paper, one year since the introduction of Supernets, there are more than 100 Supernets candidate projects, many of them under active development. Based on this, the proposed growth scenarios for Supernets seem realistic, especially given that Supernets’ deployment should become significantly easier once the Staking Layer (described in § 6) is introduced. Additionally, it is noticeable that the trend of interest in Supernets is stronger in relative terms than the one for public chains. For this reason, we are assuming the same for the proposed growth scenarios. To further justify this, a meaningful parallel with Web2 adoption history can be drawn. In the earlier days of Web2, shared application hosting – Web2 equivalent to public chains – was much more common than nowadays. As the industry matured, 9 Source: https://www.appbrain.com/stats/number-of-android-apps 8 Source: https://www.apple.com/newsroom/2022/04/report-finds-third-party-apps-see-global-success-on-the-app-st ore/ 7 Source: https://polygonscan.com/chart/tx

dedicated hosting – Web2 equivalent to Supernets – became the norm for every application with a meaningful user base and level of activity. Again, the number of Polygon chains is an abstract concept in our model; in conjunction with the number of transactions per chain, it should primarily reflect the level of economic activity in the ecosystem. Similarly, the prevalence, i.e. ratio of Supernets compared to public chains, is an abstract, conservative assumption. If it would turn out that public chains are more popular relative to Supernets, the results of the simulation presented in § 9.4 would look similar or better, due to their respective transaction fee levels. To complement the aforementioned growth scenarios, we estimate the following inputs: ● Initial supply of 10 billion POL, as described in § 5.1; ● Yearly emission rate of 1% for validator incentives, as described in § 5.2; ● Yearly emission rate of 1% for the Community Treasury, as described in § 5.2; ● $5 average POL price during the 10-year period; ● 38 transactions/second on average per public chains, comparable to current Polygon PoS chain usage10; ● 19 transactions/second on average per Supernet, an estimate based on the requirements of Supernet projects; ● $0.01 average transaction fee on public chains, an estimate based on current average fees on Polygon PoS chain;11 ● $0.001 average transaction fee on Supernets, conservative estimate given abundant blockspace and a “race to the bottom” that it will likely cause for transaction fees; ● 100 validators on average per public chain, equivalent to the current validator set size of Polygon PoS; ● 15 validators on average per Supernet, based on requirements and realistic needs of Supernet candidates; ● $6,000/year average running costs per validator, equivalent to current Polygon PoS data, gradually decreasing according to a modified version of Moore’s Law (50% decrease in 3 years). It is worth noting that POL price, although one of the required model inputs, directly and significantly affects only the Community Treasury inflow, not the other key performance indicators. Also, transaction fee estimates do not account for the cost of data availability on 11 Source: https://polygonscan.com/chart/gasprice

Source: https://polygonscan.com/chart/tx

Source: https://polygonscan.com/chart/tx

Ethereum for Polygon chains that use the rollup model; we ignore this cost because it is passed to Ethereum. 9.3 Methodology We define a simple model to estimate the key performance indicators of the ecosystem, and validate the hypothesis from § 9.1. The key indicators and the methodology to determine them are as follows: ● Staking ratio ( ): The portion of the POL supply staked by validators. 𝑆𝑟 𝑆𝑟= 𝑆𝑠 / 𝑆𝑡 Where is staked supply, i.e. total amount of POL staked by validators, and is total 𝑆𝑠 𝑆𝑡 supply, i.e. current supply of POL. ● Validator emission incentives ( ): Yearly validator incentives that come from POL 𝑉𝑖𝑖 emission. 𝑉𝑖𝑖= 𝑆𝑡 × 𝐼𝑣 × 𝑃 Where is total supply, is yearly emission rate for validator rewards and is POL 𝑆𝑡 𝐼𝑣 𝑃 price. ● Validator fees incentives ( ): Yearly validator incentives that come from gas fees. 𝑉𝑖𝑓 𝑉𝑖𝑓= 𝐶𝑝 × 𝑇𝑝× 𝐹𝑝 + 𝐶𝑠 × 𝑇𝑠× 𝐹𝑠 Where is number of public chains, is number of transactions per public chain, 𝐶𝑝 𝑇𝑝 𝐹𝑝 is average transaction fee per public chain, is number of Supernets, is number of 𝐶𝑠 𝑇𝑠 transactions per Supernet and is average transaction fee per Supernet. 𝐹𝑠 ● Validator running costs ( ): Cumulative yearly running costs of all Polygon validators. 𝑉𝑐 𝑉𝑐= (𝑁𝑝 × 𝐶𝑝+ 𝑁𝑠 × 𝐶𝑠) × 𝑌 Where is number of validators per public chain, is number of public chains, is 𝑁𝑝 𝐶𝑝 𝑁𝑠 number of validators per Supernet, is number of Supernets and are yearly running 𝐶𝑠 𝑌 costs for a single validator. ● Return on Work ( ): Total validator earnings expressed as a percentage of the value 𝑉𝑟 of staked POL. 𝑉𝑟= (𝑉𝑖𝑖 + 𝑉𝑖𝑓 − 𝑉𝑐) / (𝑆𝑠 × 𝑃)

Where are validator issuance incentives, are validator fee incentives, are 𝑉𝑖𝑖 𝑉𝑖𝑓 𝑉𝑐 validator running costs, is staked supply and is POL price. 𝑆𝑠 𝑃 ● Community Treasury inflow ( ): Total yearly inflow to the Community Treasury. 𝑋𝑖 𝑋𝑖= 𝑉𝑖𝑖= 𝑆𝑡 × 𝐼𝑡 × 𝑃 Where is total supply, is yearly emission rate for the Community Treasury and is 𝑆𝑡 𝐼𝑡 𝑃 POL price. 9.4 Results The model accepts the required inputs and processes them using the presented methodology. The results for varying input sets can provide interesting insights into the ecosystem and its dynamics, including but not limited to: ● The attractiveness and sustainability of validator incentives; ● The amount and dynamics of the the Community Treasury inflows; ● The structure of validator incentives and their changes over time; ● The effect of price on all observed indicators; ● The effect of different adoption levels to all observed indicators etc. Here we run the model with the inputs provided in § 9.2 and observe the three indicators required to validate our initial hypothesis: staking ratio ( ), validator incentives ( ) and treasury 𝑆𝑟 𝑉𝑖 inflow ( ). 𝑋𝑖 Based on the model results, we are reasonably confident that the described POL-powered ecosystem can meet all three goals outlined in § 9.1: ● Sufficient ecosystem security: We fixed the staking ratio ( ) at 30% and ran the 𝑆𝑟 model. Given that the remaining two indicators – validator incentives ( ) and treasury 𝑉𝑖 inflow ( ) – are showing expected or higher than expected values, we conclude that the 𝑋𝑖 staking ratio should retain satisfactory or higher than satisfactory levels. ● Sufficient validator incentives: The results show that the targeted Return on Work ( ) 𝑉𝑟 of 4-5% is realistic to expect. Moreover, it reaches ≈7% for medium growth and ≈10% for fast growth scenario. In reality, this would likely cause the staking ratio to increase (thus further increasing security of the ecosystem), until the market determines the equilibrium between staking ratio and returns.

● Sufficient ecosystem support: The results show that the minimal satisfactory level of the Community Treasury inflows ( ) of $50-100 million per year is realistic to expect. 𝑋𝑖 Moreover, it reaches significantly higher levels towards the end of the 10-year period. However, the treasury inflow is directly related to the price of POL, and thus highly speculative. If the treasury ends up having more funds than the ecosystem realistically needs, the community might decide to burn the excess POL, as mentioned in § 7. Figure 4. Return on Work and Community Treasury inflow The full model is open-source and can be accessed on GitHub, and used to produce and analyze results for arbitrary sets of inputs. 10 Conclusion The vision behind Polygon is to build the Value Layer of the Internet. To achieve this vision, the redesigned Polygon protocol architecture introduces a novel, infinitely scalable and seamlessly interconnected network of Layer 2 chains. In this paper, we introduced POL, the proposed native token of Polygon, designed to secure, coordinate and align the Polygon ecosystem and supercharge its growth. The proposed design and tokenomics of POL achieve the rigorous design goals that we defined. We created a model to simulate the key performance indicators of the POL-powered ecosystem, provided required model inputs and analyzed the results of the simulation. The results confirmed the hypothesis of the model, derived from the aforementioned design goals.

Based on everything above, we conclude that POL is a novel, next generation asset that provides a solid foundation for Polygon to achieve its ambitious vision.

Frequently Asked Questions

- What is the Polygon whitepaper?

- The Polygon whitepaper describes a framework for building and connecting Ethereum-compatible blockchain networks. Originally known as Matic Network, it evolved from a Plasma-based sidechain into a comprehensive multi-chain scaling platform.

- Who wrote the Polygon whitepaper and when?

- The Polygon (Matic) whitepaper was authored by Jaynti Kanani, Sandeep Nailwal, and Anurag Arjun in 2019. The project rebranded from Matic Network to Polygon in February 2021 to reflect its expanded multi-chain vision.

- What is Polygon's core technical innovation?

- Polygon provides a modular framework for Ethereum scaling with multiple solutions: the Polygon PoS sidechain, Polygon zkEVM (zero-knowledge rollup), and the CDK (Chain Development Kit) for creating custom ZK-powered L2 chains — all unified by the AggLayer.

- How does Polygon's consensus mechanism work?

- Polygon PoS uses a modified Tendermint BFT consensus with a Heimdall layer for validator management and Bor for block production. Validators stake POL (formerly MATIC) tokens and are selected for block production based on stake weight.

- How does Polygon differ from other Layer 2s?

- Polygon offers a suite of scaling solutions rather than a single approach. Its PoS chain operates as a commit chain with its own validator set, while Polygon zkEVM provides true ZK rollup security inheriting Ethereum's guarantees.

- What is Polygon's supply model?

- POL (successor to MATIC) has a supply of 10 billion tokens with a 2% annual emission for ecosystem incentives. POL serves as the native gas token for Polygon chains and can be staked for validator rewards across multiple chains.

- What are Polygon's primary use cases?

- Polygon is used for DeFi (Aave, Uniswap deployments), gaming (Immutable zkEVM), enterprise solutions (Starbucks, Nike, Reddit), NFTs, and identity. Its low fees make it ideal for high-frequency, consumer-facing applications.

- What problem does Polygon solve?

- Polygon solves Ethereum's high gas fees and limited throughput for everyday applications. It provides near-instant, low-cost transactions while maintaining compatibility with Ethereum's tooling, liquidity, and developer ecosystem.

- How does Polygon's security model work?

- Polygon PoS has its own validator set (100+ validators) with staked POL as security. Polygon zkEVM inherits Ethereum's security through zero-knowledge proofs — every transaction batch is verified by Ethereum L1 smart contracts.

- What is the current state of the Polygon ecosystem?

- Polygon has migrated from MATIC to POL as its native token, launched the zkEVM mainnet, and introduced AggLayer for unified liquidity across Polygon chains. It hosts thousands of dApps and has major enterprise partnerships.